This document proposes a basic income for the U.S. in the form of a negative income tax (NIT).

It proposes an income floor for all adults (18+) in the economy of $13,000 per year, indexed to the federal poverty line. This proposal leaves aside the question of how best to include minors, but no basic income is complete without either a reduced rate income floor for minors, or a child allowance passed alongside.

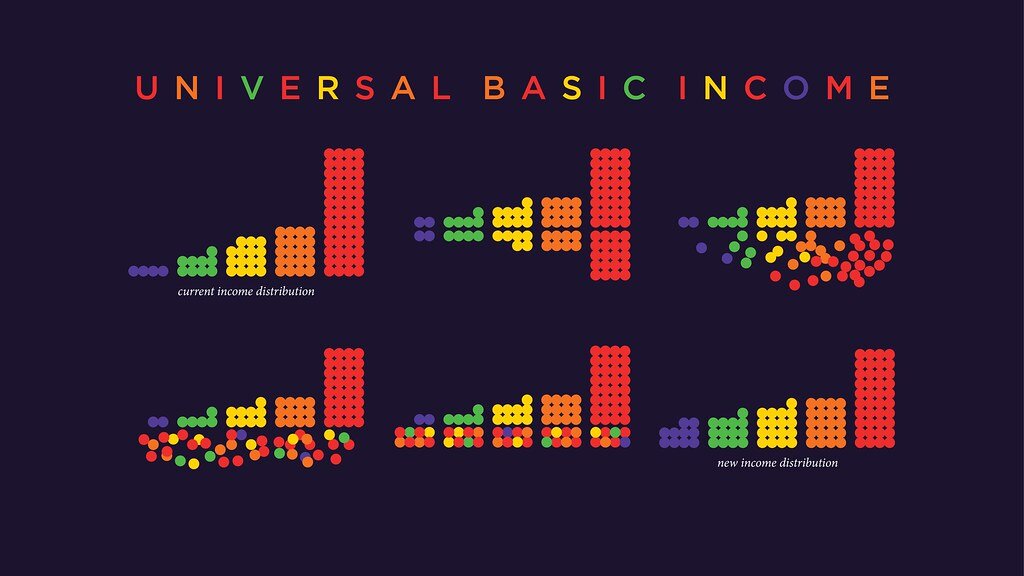

Under this proposal, an adult earning $0 annually receives the full $13,000. As their earnings increase, their NIT benefits are phased out with a 33% tax rate, zeroing out benefits for incomes beyond $39,400. Benefits would be provided in monthly installments.

Such an NIT is both economically and politically feasible. Within a year of passing, it could eliminate official poverty, increase the circulation of capital throughout the economy, reduce inequality, and insulate a basic degree of livelihood from potential shocks such as loss of employment, automation, pandemics, or changing life circumstances.

In the longer term, a basic income improves the conditions for social innovations to occur alongside technological ones. Raising the economic floor lowers the risks associated with experimental behavior. It lifts everyone towards a threshold of financial security beyond which we have more freedom to decide how to spend our time. This kind of free time, contrasted with time that must be spent working for money, is fertile soil for innovation.

Moving towards collective liberation from the strictures of economic anxiety could provoke an upsurge in the kinds of broader innovation we need to meet the spectrum of challenges facing our civilization. Economic freedom is an intersectional catalyst towards ecological, racial, feminist, and mental freedoms.

I calculate this NIT would cost $855 billion per year. My funding proposal details two primary categories of revenue: reforming and eliminating existing welfare and tax programs ($346 billion), and implementing new progressive taxes ($744 billion). Together, these reach a total funding capacity of $1.09 trillion, $235 billion above my funding estimate. Crucially, the plan does so without raising the tax burden on most Americans.

What Is a Negative Income Tax?

NIT is a targeted basic income that phases out as one’s earnings increase. It’s composed of two variables: an income floor, and a phaseout tax rate. The income floor sets the amount an individual with $0 of annual income receives from the program: the maximum benefit amount one can receive from the NIT.

The phaseout rate determines how much of the NIT is phased out for each dollar of earned income. The lower the rate, the larger the category of people who benefit from the NIT program, and the more work incentives are preserved (because earning additional income loses you less of the NIT benefit). But the higher the programs cost. Conversely, higher rates mean fewer people benefit and incentives for low-wage work are decreased. But the cost is lessened.

Together, the phaseout tax rate and the income floor create a third element: the breakeven point. This is the earnings level at which NIT benefits are fully phased out to $0.

Why a Negative Income Tax

How is it that in a society as wealthy as ours, economic anxiety remains the prevailing reality for so many? This question has vexed economists at least since Henry George in the late 1800’s. In our time, after centuries of vigorous capital accumulation, we are past due to leverage our wealth to provide a basic income that reduces the hold economic insecurities have upon our lives, behaviors, and minds.

NIT is both an economic and politically feasible way to implement this basic income. It’s a policy with immediate and obvious effects, followed by more subtle, and perhaps profound ones.

Within a year of passing, NIT could:

Eliminate poverty by setting the income threshold above the federal poverty line

Reduce inequality and increase the circulation of capital throughout the economy by redistributing wealth from its accumulation at the top back towards lower income groups who are more likely to spend it

Increase the bargaining power of workers by increasing their ability to meet their basic needs outside of employment, empowering them to more readily reject undesirable or exploitative labor contracts

Guarantee and protect a basic degree of livelihood from potential shocks such as loss of employment, automation, pandemics, or changing life circumstances.

But the long-run effects reach much deeper into the core of our social relations, ways of living, and modes of innovation. With a basic income, the risk attached to experimental behavior is greatly reduced. The spectrum of viable behaviors - ways of living, even - is increased. Unconditional income enables those who’d prefer spending more of their time engaged in unpaid activities, that they nevertheless consider valuable, to do so. As a society, we gain optionality. The ways of participating in society people consider legitimate is expanded, as recent interviews with UBI recipients from a Finnish experiment confirm.

The diversity (and redistribution) of ‘free time’ is precisely the point. Free time is unbound from the imperative to earn, from the necessity to please bosses, deadlines, or metrics. It’s time in which we can do things for themselves. The quality of thought that occurs for itself, as opposed to for a job, is notably different. More autonomous. Charles Darwin, after all, produced his theory of evolution in his free time.

The innovations that spring from free time arise from a different kind of investment. Unbound from the imperative to earn, they can address a broader scope of human concerns. These socialinnovations function alongside technological ones that arise from market incentives, contributing a broader range to the scope of innovation.

But perhaps the most urgent motivation to establish a basic income is because doing so would make an immediate difference in the everyday lives of ordinary people. People who’ve been left out of the gains from the extensive capital accumulation their labor contributes to.

Payment Details

This proposed NIT sets the income floor at $13,000 (rounded up from the 2020 poverty line of $12,760) and uses a 33% phaseout tax rate. The breakeven point beyond which benefits reach zero is $39,393.

The chart below shows how much NIT benefit one would receive at different levels of income:

This proposal does not cover a plan for minors. But it is absolutely vital to the efficacy of the program that such a plan is concurrently passed.

Most basic income proposals include a reduced rate for minors, often hovering around 50% of the adult level. This approach is not without oddities. Especially in the context of a NIT rather than UBI. For example, since almost none of the 74 million minors in the US earn income, and even fewer earn anywhere near a hypothetical reduced income floor of $6,500, almost all children - including those of eminently wealthy families - would receive the full benefit.

So even though the program is considered a NIT, it amounts to only an NIT for adults, but a UBI for minors.

It may be preferable to complement a NIT for adults with a child allowance that phases out benefits as guardians’ earnings increase. In this way, just as NIT benefits phase out before going to wealthier adults, benefits would phase out for minors higher up the wealth distribution as well.

However, some argue that children constitute a “public good”, and child allowances should be universal. I leave this debate untouched, trusting that either method - a reduced rate NIT income floor, or a child allowance (universal or otherwise) - complement and fulfill the motivations behind this basic income proposal.

In terms of cost, some child programs are budget neutral, while the higher end of cost estimates reach up towards $200 billion.

How Much Would This NIT Cost?

I calculate this NIT, provided in 2018 to all adults over the age of 18 would’ve cost $855 billion.

In addition to my own calculations, I use four existing cost estimates for similar programs to establish a spectrum of potential costs. This spectrum runs from $539 billion to $1.09 trillion:

Each plan slightly differs, but taken together, they create a spectrum to anchor our cost expectations. But details make all the difference. For example, the disparity between Widerquist and Santens’ estimates derives largely from differences in assumed tax rates. Wiederspan et. al’s NIT proposal is for household, rather than individual income. And Philip Harvey’s estimate was set at the poverty line with a 25.6% phaseout rate, with numbers given in 2002 terms.

For the present proposal, I calculated the cost using 2018 data from the current population survey. It gives the distribution of personal incomes in increments of $2,500, providing the quantity of individuals in each earning bracket. For each bracket, I took the middle of the bracket as the income for that group. For example, for the 11,090,000 individuals in the income group between $0 - $2,500, I treat their income as $1,250.

Since cost estimates must use income data from the economy without a basic income, we must take all estimates loosely. They cannot account for how introducing a basic income would lead to a change in behaviors and earned incomes that would alter the actual cost of the program. Whether we expect the cost to increase or decrease in response to these changes is unclear. There exist clear knock-on effects in both directions.

How to Pay for NIT

For my funding calculations, I chose to use Philip Harvey’s $1.09 trillion as the funding target rather than my own. I do so to demonstrate that whatever the cost, an achievable funding proposal is well within reach.

Funding Summary

A $1.09 trillion NIT program could be funded through two categories of funding. First, eliminating or reforming existing welfare and tax programs. Second, implementing new progressive taxes.

We could eliminate redundant welfare programs such as the earned income tax credit, supplemental security income, supplemental nutritional assistance program, and temporary assistance for needy families (total revenue of $198 billion). We could eliminate wealthy-favoring tax programs like the mortgage interest deduction and the real estate tax deduction ($89 billion). And we could reduce the defense department’s budget by 10% ($59 billion).

In total these provide $346 billion towards the cost. I then offer two strategies for approaching the remaining $744 billion via progressive taxation.

We may either enact one single, large tax, or we may prefer implementing a series of smaller progressive taxes. Options for the single tax include a value added tax (raising $600 billion - $1.3 trillion in new revenue depending on exclusions), or an adaptation of Saez & Zucman’s proposed national income tax that draws upon both labor and capital. They estimate a 6% flat rate could raise $1.2 trillion. I estimate phasing the tax in on incomes above the NIT breakeven point to a top rate of 5% would be sufficient to cover the remaining $744 billion.

For the series of smaller taxes, we could fully fund the NIT with: progressive top income tax rates ($18.9 - $70 billion), carbon tax ($100 - $210 billion), wealth tax ($118 - 375 billion), financial transaction tax ($70 billion), and raising the effective corporate tax rate ($235 billion).

Funding Details

Repurposing Existing Programs

A sizable portion of the expense can be offset by folding existing welfare programs that a NIT would make redundant. These programs might include: the earned income tax credit ($59 billion), supplemental security income ($58 billion), supplemental nutritional assistance program ($64 billion), temporary assistance for needy families ($16.7 billion).

It’s crucial to emphasize, however, that NIT must not replace welfare, but place it on firmer ground. An NIT that replaces all other welfare programs (of the variety Milton Friedman or Charles Murray advocate) would have harmfullyregressiveoutcomes. The programs listed above are means-tested, meaning most recipients would naturally be elevated above their eligibility requirements anyway.

Together, these programs would provide $198 billion towards the total cost.

In addition to these reforms, we spent $540 billion in 2013 on “tax programs”: tax credits, deductions, exclusions, exemptions, deferrals, and reduced rates, most of which overwhelmingly benefit the wealthy. Indeed, these tax programs are known as “asset building” programs, lowering the tax rates on capital so that wealth can accumulate.

But in 2013, we spent over $100 billion more on these asset building tax programs than we did the entire welfare program budget (excluding medicare/medicaid):

These tax programs, which function as federal expenditures, can be reformed to better serve most Americans, and to help offset the cost of a NIT. For example, eliminating the home mortgage interest deduction - an idea with bipartisan support - is estimated to save $59.7 billion per year. Similarly, eliminating the real estate tax deduction would have freed up $29.3 billion in 2013.

Together, eliminating these two programs alone could contribute $89 billion annually, leaving a mass of wealthy-favoring tax programs still in place.

Finally, we may consider reducing the defense department's budget by 10%, yielding an additional $59 billion, annually.

Combining all of these tax reforms, we so far have $346 billion available in annual funding for the NIT:

The remaining $744 billion can be raised through a variety of progressive taxes.

There are at least two strategies for progressive taxation reform to achieve $744 billion in additional revenue. We may either look to enact a single, large tax, such as a value added tax, or a national income tax. Or, we may prefer enacting a series of smaller progressive taxes - such as a carbon tax, financial transaction tax, wealth tax, higher top income tax rates, and higher corporate tax rates.

One Large Tax

I’ll offer two single tax options. The value added tax (VAT) is familiar to most of the developed world (166 of 193 countries with UN membership have one in place). Some economists worry, however, that it’s a regressive tax suited more to the 20th century economy than the 21st.

As a progressive alternative to the VAT tax, economists Gabriel Zucman and Emmanuel Saez proposed a national income tax in their 2019 book, drawing upon both labor and capital income. They describe it as a way to “leapfrog the VAT”, paving the way in creating “fiscal institutions of the twenty-first century.”

Value Added Tax

A 10% VAT tax is projected to raise approximately $600 billion per year, whereas the same 10% VAT applied to a broader base of goods is estimated to raise up to $1.3 trillion per year.

Empiricalstudiesare increasingly finding that a VAT is regressive (hits those with lower incomes harder than those with higher incomes), though debate remains as to precisely how regressive. Some UBI proposals account for this regressivity by setting the payout level - or in our case, the NIT income threshold - $200 above the poverty line.

Alternatively, a basic income can justify reducing the social security tax rate. Since social security is essentially a basic income for seniors, there’s less need to maintain its payout levels going forward, since they’ll be receiving basic income from the NIT program. Lowering the tax rate will lead to lower future benefit levels (without robbing those who’ve already paid into the program of their due benefits), but the basic income will more than make up the difference. This decreased tax rate on all (for example, from 6.2% to 4%) can help offset additional costs the VAT passes on to consumers.

National Income Tax

The national income tax was proposed as a 6% flat tax on all income, labor and capital, with no exemptions or deductions. In their proposal, Saez and Zucman (2019) estimate $1.2 trillion in annual revenue.

Adapting this tax to the NIT, I calculate a 5% national income tax phasing in on earnings above the breakeven point of $39,393 would be sufficient to fund the remaining $744 billion.

Originally, the negative income tax proposed by Milton Friedman was funded in quite a similar manner. Friedman wanted to keep it simple: If you earn below the breakeven point, you receive money. If you earn above it, an income tax phases in to fund the program.

But as we learn more about the nature of income and wealth inequality, it’s clear that the wealthy make most of their income via capital income, while working classes rely on wages. Therefore, an income tax applied only to labor incomes hits working classes much harder than the wealthy. Applying the tax to all forms of income means the wealthy pay the same proportion of their real incomes towards the program as everyone else.

The primary challenges to this approach - intuitive as it may seem that the wealthy shouldn’t get to pay a lower percentage of their overall income than others - are fiscal manipulation and capital flight. The tax would effectively raise rates on corporate profits, incentivizing the movement of money abroad. International tax competition, which has become one big race to the bottom, makes this sort of taxation tricky.

Accordingly, as Saez and Zucman acknowledge, the successful implementation of this kind of tax requires reforming our approach to the taxation of multinational corporations. Incidentally, Zucman wrote both a book and a policy brief on doing just that.

A Smaller Series of Taxes

If the VAT is too regressive, and the national income tax proves infeasible for the time being, we may prefer to use this as an opportunity to implement a series of smaller taxes that raise revenues while adjusting the economy’s architecture to better serve the majority of the American people, the planet, and our collective pursuit of progress.

Progressive Marginal Income Tax Rates

Recent research suggests the revenue maximizing top tax rate on incomes falls between 68 - 73%. Presently, our top tax bracket is 39.6% on earnings above $400,000. Much debate has ensued over the question of raising top marginal income taxes, largely spurred by Saez & Zucman’s recent finding that in 2018, the wealthiest households paid a lower tax rate than the poorest:

Revenue estimates for raising the highest income tax rates vary from $18.9 billion, up to $70 billion annually, largely dependent upon the broader environment of tax policy.

It’s worth noting that the US pioneered high marginal income tax rates throughout the mid-20th century. Top rates reached above 90%, with effective rates sitting closer to 50%. There’s nothing unprecedented about proposing a return to higher marginal income tax rates.

Wealth Tax

Projected revenues: $118 billion - $375 billion.

A 2% tax on wealth above $50 million, cranking up to 3% on wealth above $1 billion, is projected to raise $275 billion, annually.

There are two important elements to the debate over carbon tax. First, a successful carbon tax would yield diminishing revenues, moving towards zero. Second, there’s a design question: a carbon tax sets a price on carbon and lets emissions calibrate organically, while a cap-and-trade approach sets an emissions level and lets prices calibrate organically.

379 of the Fortune 500 companies paid an effective federal tax rate of 11.3% on their 2018 income, 9.7% less than the actual corporate tax rate of 21%. 91 of those corporations - including Amazon, Chevron, IBM - paid $0 in taxes on their 2018 income.

Reforming the corporate tax rate - largely by reconsidering deductions, allowances, and loopholes - can help raise the actual rates they pay closer to the stated tax rates they’re meant to. In 2017, a perfect application of the 21% corporate tax rate would’ve raised $421 billion. Actual revenues from the corporate income tax in 2017 were $297 billion.

But changing the stated rate matters too. The 2017 tax cuts reduced the corporate tax rate from 35% to 21%, leading to a $135 billion decline in revenue.

Financial Transaction Tax

Projected revenues: $70 billion

A FTT, beyond raising revenue, has a significant corrective effect on the unbridled incentives of the finance industry. By discouraging high-frequency, short-term trading, a FTT discourages the short-termism that has plagued the economy since deregulation loosened capital controls in the 1970’s.

Summation

The series of taxes listed above are projected to raise between $542 billion - $960 billion. Our required revenue of $744 billion falls nicely in the middle. Further options exist, such as raising capital gains taxes, eliminating more ‘asset building’ tax programs, rental fees on natural resources (such as the Alaskan model of taxing oil revenues to provide a partial basic income to all citizens), or financing a portion of the cost through deficit spending.

Administration

The actual administration of the NIT - scaling benefits appropriately with fluctuating incomes on a monthly basis, and distributing those payments to all recipients - presents both obstacles, and opportunities. Presently, we struggle enough with reporting our incomes annually. It is difficult to imagine citizens reporting their incomes monthly, in order to receive appropriately sized NIT checks.

But we’re well overdue to redesign our income and tax reporting systems in light of the latest digital technologies and platforms. We certainly don’t lack the public interest, nor political will, to simplify tax reporting systems.

Consider, for example, a digital income reporting platform that each citizen is responsible for updating monthly (better yet, remove the friction by automating the process, so that any income earned automatically registers on this ledger). Monthly NIT payouts can adjust in response to these income declarations. Then, when we do our annual taxes as usual, our official annual incomes are available to resolve any discrepancies.

Individuals who under-report their incomes on the monthly platform, therefore receiving more NIT than they should, can pay it back in the form of a tax penalty (and perhaps with an additional fine, disincentivizing systematic underreporting to effectively treat extra NIT payouts as a line of credit).

Barring a new digital income reporting infrastructure, there still exist feasible options. First, as economists of all stripes agree, from Milton Friedman to Thomas Piketty, the ideal place to provide NIT benefits and tax adjustments is directly on one’s paycheck. In the same way that each paycheck lists federal tax deductions, it can list one’s NIT benefits (and tax contributions) applied to that very check. But this method may grow more difficult as work itself evolves, and the ways in which we earn income transition from single-employer careers to kaleidoscopic, diversified models.

If the evolution of work prevents paychecks from providing the bulk of NIT calculations, we can still adopt an income declaration system using existing platforms. In the same way that unemployment recipients must actively “claim” weekly benefits, receiving monthly NIT could depend on actively reporting one’s income to the NIT administering agency, such as the IRS. In the same way as above, we can adjust for any discrepancies when we do our annual taxes, using fines and penalties to discourage exploitation.

Requiring recipients to actively report their incomes also builds in a frictionless ‘opting-out’ method for all those who don’t expect to receive any NIT benefit. Someone earning $200,000 annually, well over the breakeven point, would be required to take no action. By default, no one receives NIT. So only those who expect to receive payments would ‘opt-in’ by self-reporting their income. This naturally reduces the bureaucratic load.

In a proposal for a social wealth fund, The People’s Policy Project provides a visual aid that models a potentially digitized NIT platform nicely.

Atop the left screen where “value of your share” is listed, this could be the space where one’s reported income is shown. The screen on the right, rather than showing one’s “dividend redemption”, could show the NIT benefit to be deposited into the recipients account that month.

Just as Saez & Zucman see the implementation of a national income tax as an opportunity to bring our tax system into the 21st century, digitally reporting incomes provides an opportunity to update how we do our personal taxes.

Next Steps

Two major obstacles to implementing an NIT are the lack of rigorous funding and administration proposals. Here, I offered suggestions for both, upon which I hope more capable researchers will build.

There is also a lack of research into optimal phaseout tax rates. I use 33% because it’s the lowest rate commonly used in existing NIT research. But the lower the rate, the more people benefit from the NIT, and the more potent it becomes as a vehicle for robust change. Research is needed to explore the lowest sustainable phaseout rates.

This leaves four next steps:

Debate over the most appropriate funding model

Determine best approach for minors: cash allowance, or reduce income threshold?

Develop income reporting & payment distribution methodology

Research optimal NIT phaseout rates

Whatever disputes may arise over implementation details, it’s crucial to remember that all advocates of basic income - whether UBI or NIT - stand on common ground. Broader still, this common ground extends beneath the entire sweep of policies seeking to leverage our collective wealth to directly alleviate economic insecurity for all.

Rather than waiting for aggregate-GDP growth to fulfill the neoliberal promise - where economic growth is said to do more for human well-being than any direct interventions can - we can immediately begin providing what a recent proposal for universal basic services calls “a larger life for the ordinary person”.

Cutting everybody directly into the fruits of capital accumulation increases optionality for those with lower incomes in the same way that wealth does for those with higher incomes. This allows for greater diversity in what we do with our time, how we organize our lives, and ultimately, the kinds of wealth and value society produces.

A negative income tax of the variety proposed here offers a crucial piece of the puzzle for an immediate, direct, and feasible strategy towards actualizing these possibilities today, in our time.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

A Negative Income Tax for the 21st Century

Oshan Jarow - May 9th, 2020

The purpose of this document is to facilitate sense-making on what’s become a complex, tribal, and absolutely vital subject of debate: universal basic income (UBI).

Think of this as a not-so-brief policy brief. A policy long, if you will. What policy briefs offer in brevity and distillation, they sacrifice in complexity and nuance. UBI’s surging popularity is producing an abundance of briefs, but a scarcity of longs. Briefs present fixed ideas, whereas longs reveal the flux and uncertainties beneath them.

Ironically, I only encountered UBI after receiving a degree in economics. I spent the next 5 years studying UBI, and the broader terrain of economic thinking that’s usually left off university curriculums.

Regarding UBI, I’ve occupied every position along the spectrum. I’ve been the starry-eyed supporter enthralled to its promises, and I’ve been the disillusioned skeptic, dismissing UBI as a well-intentioned, but naive lurch for utopia.

My hope is to provide an easy-to-navigate document that offers exposure to the many questions and conflicts driving the UBI debate. Hopefully, by offering the depth so many UBI puff-pieces lack, this policy long might help unsteady some of our fixed ideas, and lead us deeper into the labyrinth of considerations a UBI provokes.

Here’s a map of what’s covered below. Feel free to click & jump around to whatever interests you:

After exploring each of these areas in relative depth, I’ll conclude with a broader sentiment: economic insecurity has a dampening effect on human consciousness. The world is far more mysterious, wonderful, and stimulating than human perception can grasp, but economic insecurity further inhibits our capacities, like a horse with blinders on.

Despite being surrounded on all sides by enchantments, our lives are too often squandered in forms of suffering and anxiety that, in the 21st century, are preventable. The motivation behind UBI is one we all share: it’s time to build a better world. The motivation behind policy analysis is to ask: would UBI move us in that direction?

I recently published an in-depth exploration of the impact UBI might have on human development, consciousness, and social complexity. You can read that essay here.

What is Universal Basic Income?

UBI is an unconditional cash payment provided to all citizens, in an amount sufficient to meet their basic needs, on a (minimum) monthly basis. Most proposals include a reduced rate for minors.

Universal: Given to every individual, regardless of employment status, earnings, or demographic.

Basic: Sufficient to meet basic needs

Income: cash.

How Much is "Basic"?

The most common UBI amount - $1,000 per month - is based on the federal poverty line. The 2019 poverty line was $12,490, or $1,041 per month. Equating “basic” with the poverty line is consistent with the work of seminal economists and philosophers such as Amartya Sen and Martha Nussbaum.

Pinning the UBI amount to the poverty line requires adjusting the payout level for both inflation, and changes to how we define poverty.

How Much Would UBI Cost?

UBI has two relevant costs, gross and net. The gross cost reflects the total revenue the government must raise to fund the program. The net cost reflects the actual expense to taxpayers.

Since funding a poverty level UBI requires progressive taxation, an upper portion of recipients will wind up paying more in new taxes than they receive from UBI. This creates a canceling out effect, where one receives $12,000 in UBI, but pays $14,000 in higher taxes. The effective cost to them is $2,000, rather than $14,000. The cost of UBI that takes these cancellations into account is the net cost.

The gross cost of a UBI equal to the poverty level in 2019 ($12,490) for all citizens above 18 would’ve been $3.2 trillion. Adding a 50% UBI for minors would increase the gross cost to $3.6 trillion.

Moving from gross to net cost is difficult to forecast, as it depends on the specific taxes used to fund it. But we can establish a range for the net cost from existing estimates. Political philosopher Karl Widerquist used a series of simplified assumptions to calculate the net cost of a $12,000 UBI for adults and $6,000 for children, totaling a gross cost of $3.42 trillion. His estimates yielded a net cost of $539 billion, or 15.7% of the gross cost.

On the upper bound of the spectrum, economist Philip Harvey estimated the net cost of a similar - though not identical - UBI at $1.69 trillion.

Why UBI?

Elsewhere, I’ve written on the philosophy of UBI, exploring it as a means of decommodifying time and diversifying human development. But in popular discourse, there are at least six categories of motivation for UBI:

I. Immediately ending official poverty in the US II. Reducing the imbalance of power & wealth between labor & capital III. Boosting demand by raising purchasing power of lower income groups IV. The threat of automation & detaching a basic amount of livelihood from labor V. Improving markets by providing for basic needs outside of markets, making remaining exchanges more voluntary VI. Beginning to implement the cultural conditions for 'post-scarcity'

Automation

“There is no reason why in a society which has reached the general level of wealth which ours has…that the security of a minimum income should not be guaranteed to all without endangering general freedom.”

— F.A. HAYEK

Automation is simultaneously the easiest narrative to stir up support for UBI, and the weakest one to build it upon. There is no critical consensus as to whether impending waves of automation will be any different than ones we’ve witnessed throughout history. Whether or not automation lives up to the hype, the case for UBI remains.

But there's a nuance in this argument worth pulling out. How will automation benefit society? How can we distribute and democratize the gains? How do we keep society from devolving into a class struggle between those who own the robots and those being replaced by them?

The question of who benefits from automation is firstly a question of power. If we’re concerned with power dynamics within firms, we can explore policies like codetermination, where worker representatives are given direct seats on company boards. This gives workers’ interests direct voting power in company decisions. Democratizing decision making power changes how productivity gains are implemented and realized in the first place, rather than relying on redistribution to take care of those who are left out of the gains.

But the sentiment of detaching labor from livelihood goes beyond automation. Since at least the 1800’s with Henry George’s Progress and Poverty, the stubborn tendency for wages to remain at the minimum that affords subsistence despite massive gains in capital accumulation has raised questions. As our accumulated wealth increases, why can we not guarantee a basic degree of livelihood irrespective of labor?

The case for UBI in this dynamic is best presented by a dialogue across 150 years, between George and the great novelist Marilynne Robinson. In 1879, George asked: “Why, in spite of increase in productive power, do wages tend to a minimum which will give but a bare living?” A century and a half later, Robinson ventures an answer: “because they can, neither ethics nor laws intervening.”

If livelihood is to untether itself from labor, it will not occur as a natural outcome of economies informed by neoclassical economic theory. Rising tides may lift all boats, but without explicit interventions, the distance between working class wages and subsistence levels in society will remain minimal.

UBI, whether as a response to automation, global pandemic, or whatever other shocks unsteady the economy, strives to ensure a basic dimension of survival security to all. By instituting an earnings floor in the economy that lifts the bottom up, it increases the distance between the lowest wages and the subsistence level.

Poverty

“The association of poverty with progress is the great enigma of our times...From it come the clouds that overhang the future of the most progressive and self-reliant nations.”

— HENRY GEORGE, 1879

In the 21st century, domestic poverty in the US is a choice, rather than necessity. It is an outcome of policy choices (and lack thereof), rather than an enigma of progress, as it was in George’s day. And yet it rages on.

The cost of directly ending poverty for every citizen in the United States, by simply providing them a tax subsidy equal to the amount that would raise their incomes to the poverty level, would cost less than $200 billion. That’s 29% of the defense department’s budget.

Simply giving everyone exactly the amount they need to reach the poverty line creates all sorts of work disincentive problems. But the closest functional approach to formalizing that logic comes in the form of a negative income tax (NIT).

Rather than giving people the exact difference between their income and the poverty line, NIT’s use a phaseout tax rate that slowly decreases NIT benefits as earned income increases. This helps preserve work incentives and avoid poverty traps.

Incidentally, although NIT and UBI might appear quite different on the surface, the closer you look, the more difficult it becomes to tell the difference between NIT and UBI.

Economists agree that NIT and UBI would have the same net transfer effects, meaning the overall redistribution of income is identical either way. UBI gives everyone the full poverty-level amount, and then taxes some of that payout back - known as the clawback rate - from those higher in the income distribution. In UBI’s case, the clawback rate is implicit.

NIT, by contrast, adjusts payout levels to people’s incomes, avoiding the necessity to tax it back. The clawback rate is explicit. Studies suggest implicit clawback rates have psychological advantages. But the debate over which policy is preferable, UBI or NIT, is far from settled, and will hopefully come into full bloom as we commit ourselves to the eradication of poverty.

The 21st century US exhibits a confounding juxtaposition of poverty with prosperity. What Henry George wrote in 1879 is all the more true today:

“It is as though an immense wedge were being forced, not underneath society, but through society. Those who are above the point of separation are elevated, but those who are below are crushed down.”

Policies like UBI and NIT seek to reposition the wedge of progress underneath society, so that all are lifted.

Inequality

But crucially, UBI is not merely a measure to eliminate poverty. Framing UBI as just a countermeasure for poverty sells its reformative potential short, like a grandparent who uses an iPhone for nothing but phone calls.

Prior to the 1960’s, poverty was rarely considered separate from wider inequalities between labor and capital. Poverty is only the tail-end of inequality, a white-cap on the surface of a vast and deep ocean. Narrowing the focus of social reform from inequality to poverty, as sociologist Daniel Zamora wonderfully documents, was a project closely associated with the rise of neoliberal, free-market ideology.

It’s no coincidence that the first serious NIT proposal was made by none other than Milton Friedman, whose edifice of economic ideas supported the rise of neoliberal economics that dominated the period from 1972 - 2008. Zamora writes:

"In his view, a focus on “poverty” was the only reasonable social policy within a free market system. If we followed a policy that tended to reduce inequality we would inevitably affect 'the heart of the dynamism of the market economy.' A program directed specifically against poverty, on the other hand, as argued by Friedman himself, 'while operating through the market' would 'not distort the market or impede its functioning,' as did Keynesian programs.”

But at least since Thomas Piketty’s landmark 2013 book, Capital in the 21st Century (not to mention his more recent, and more ambitiousCapital and Ideology), the broader spectrum of inequality is back in the spotlight of popular discourse.

UBI critics on the progressive left are concerned that UBI, on its own, is not only insufficient to combat inequality, but might actually further entrench the forces that generate inequality in the first place.

From this angle, UBI is categorized as merely a redistributive reform, doing nothing to change the underlying dynamics that create wealth inequality, and so power inequalities, in the first place.

These criticisms are important, but partial and often misleading. UBI can be considered alongside reforms that more directly target power dynamics. However there is no reason to use an either/or framework, rather than a both/and. UBI offers a unique kind of power distribution that other reforms such as codetermination cannot.

Where codetermination democratizes power inside firms, UBI increases the bargaining power of labor from outside. This is often referred to as the power to "say no” to exploitative labor contracts. With UBI, workers have a foundation of security that allows them to more readily reject undesirable working conditions. This appeals to a broad base of economic thinking, as it’s in line with Adam Smith’s vision for “perfect liberty”.

For Smith, perfect liberty meant every worker is free to choose what job suits them best, and to change as often as they like in search of the best fit. He writes of perfect liberty as a state:

“…where every [hu]man was perfectly free both to choose what occupation [s]he thought proper, and to change it as often as [s]he thought proper. Every [hu]man’s interest would prompt him to seek the advantageous, and to shun the disadvantageous employment.”

An adequate UBI creates an environment in which workers enjoy greater fluidity between jobs, enabling their search for the right fit. But once they accept a job, UBI’s effects on power subside. Within firms, codetermination can then take over, giving workers greater say over how their places of employment make decisions.

UBI Fixes Markets

What are the necessary conditions for freedom in a market society? Prior to enclosure movements that began claiming all land under the legal jurisdiction of private property, individuals had a choice. One could participate in 'society’, whatever that entailed. Or, if society was of no interest, you were free to find a plot of land, cultivate the earth, and survive on your own.

But ever since all available land was swept up into private ownership, this ‘exit option’ is off the table. In order to access the resources we need to survive, the only choice available to most people is participating in the market economy and earning enough income to buy what you need.

Effectively, people lost the power to say “no” at a basic level. Participation in market society is the only option, and this creates opportunities for exploitation. UBI recreates the lost exit option. By unconditionally providing people enough to meet their basic needs, UBI empowers people with the means to exit exploitation.

By giving workers the power to say no, UBI provides what political philosopher Karl Widerquist calls the physical basis for voluntary trade. From a different angle, anthropologist David Graeber frames UBI as the safe-word in a safe-word theory of social liberation. By affording people the real option of saying no, of opting out of exploitation, it increases the freedom with which we can say “yes”.

Extending UBI to everyone, the social and labor relations that hold society together would be remade. People could opt out of exploitative relationships without sacrificing their basic needs. The relations that remain, and the new ones that take shape, would be based on increasingly voluntary decisions.

Without these sufficient conditions that assure all transactions in a market economy are voluntary, the entire theoretical justification of market economies collapses. Widerquist writes:

"...when neoclassical economists theorize about the world, they assume voluntary exchange is taking place. Building on this assumption, neoclassical economics goes on to conclude a variety of important results such as that market activity is efficient, that free trade has net positive effects and that markets in which economic agents participate voluntarily make them better off...Although the legitimacy of the market economy is premised on voluntary trade, without a reasonable exit option, the trading system as a whole lacks an acceptable alternative.”

We are left with two choices. Either unconditionally provide everyone with the physical basis for voluntary trade, or abandon the appeal to voluntary trade as a justification for market economies.

UBI Stimulates Demand

Whether UBI would shrink or grow the economy depends on a dazzling web of interdependent factors, making all predictions tenuous at best. As you might expect, economists have constructed models that give all sorts of contradicting reports. Some models predict UBI stimulates growth, while others expect precisely the opposite.

But most models agree on one important element: The lower one is on the income distribution, the higher the likelihood they will spend any additional dollar they receive. Conversely, the wealthier one is, the more likely they are to save each marginal dollar they receive. This has important implications for forecasting how UBI might stimulate economic activity.

Even if UBI does not increase economic growth, and functions as a pure redistribution of income from the top towards the bottom, economic activity would likely increase. Shifting money from those at the top who are more likely to save, to those at the bottom who are more likely to spend, we can expect an increase in aggregate demand. High income inequality, writes John Maynard Keynes, “causes a separation between the power to consume and the desire to consume.”

By redistributing money to where the desire to consume is highest, overall consumption will increase.

Post-Scarcity

The 2008 financial collapse stirred our socioeconomic imaginations. Business as usual lost its appeal. But what comes next? The term post-scarcity is a phrase used to gesture towards a society where scarcity is no longer the organizing principle of human behavior. As the economic historian Robert Heilbroner writes:

“For the introduction of technology has one last effect whose ultimate implications for the metamorphosis of capitalism are perhaps greatest of all. This is the effect of technology in steadily raising the average level of well-being; thereby gradually bringing to an end the condition of material need as an effective stimulus for human behavior”

Reaching all the way back to Keynes, post-scarcity refers to a society where the marginal value of capital goods drops to near zero. Consider a pencil today. We have no problems asking each other to borrow pencils. It’s considered rude, if you have extras, not to give someone a pencil who asks. And most tellingly, if you forget to give the pencil back, it isn’t a big deal.

This is because the marginal value of pencils - a capital good - is near zero. People’s lives are hardly improved by gaining additional pencils. They’re easily accessible at low costs. Keynes imagined a society where all capital goods were as common as pencils, and therefore shared with those who need them without so much as a second thought. He writes:

"The course of affairs will simply be that there will be ever larger and larger classes and groups of people from whom problems of economic necessity have been practically removed. The critical difference will be realised when this condition has become so general that the nature of one’s duty to one’s neighbour is changed. For it will remain reasonable to be economically purposive for others after it has ceased to be reasonable for oneself.”

With material goods receding to occupy a negligible portion of our aspirations (not because we somehow become less materialistic, but because everyone has abundant access to all capital goods they could want), new stimuli for human behavior would naturally emerge. Different forms of immaterial capital (social, cultural, etc) would become the focus of our energies.

UBI, a program that gives everyone a baseline of unconditional income (access to capital), begins to implement these conditions of post-scarcity. In market economies, unconditional income (for which one needn’t trade any time, labor, or money) provides immediate access goods and services we’d otherwise need to trade our time in order to receive. The more unconditional income provided, the less of one’s life-time that must be traded to acquire the goods and services we need.

This lowers the threshold of earnings required for people to meet their basic needs and, should they choose to, devote their time to unpaid activities. Human behavior becomes unbound from the imperative to earn income. Unpaid activities become more viable life-choices.

The theory of post-scarcity has to do with marginal value and rate of return on capital. But the praxis of post-scarcity shows up in the kind of cultural logic that emerges out of a society with wide-spread decreasing returns on capital goods.

As the scholar Robert Chernomas writes: “Keynes’s concern is with achieving the logic, humanity, and culture of a society that could be built only when preoccupation with economic concerns becomes unnecessary."

UBI does not achieve post-scarcity. In fact, some critics suggest the redistributional nature of UBI precludes it from ever being able to fully realize post-scarcity. Since UBI is restricted to redistributing existing wealth, it remains dependent upon a society organized around the accumulation of financial capital. If capital accumulation withers away, no longer the central stimulus driving human behavior, the overall quantity of wealth created will also shrink, reducing the available funding pool for UBI.

These criticisms are important, but not damning. While it is theoretically conceivable that a networked economy with increasing returns could actually skim off enough of those returns to fund a post-scarcity inducing UBI, in practice, this remains beyond immediate reach.

But a UBI can still create spaces of post-scarcity within the interstices of the broader capitalist system. These interstitial post-scarcity spaces allow us to begin experimenting and exploring with new ways of organizing ourselves. These shallows of experimentation, however incomplete and piecemeal, are vital for developing our imaginative capacity to design new systems.

The Problems of UBI

The more radical a proposal, the more scrutiny it should receive. Given the magnitude of UBI, in terms of both implications and costs, it merits abundant scrutiny. I’ll cover a range of critiques, responding to them where possible, and indicating those that remain unanswered.

I. UBI won't change anything II. Couldn't UBI collapse the economy? III. We'll all become lazy & dependent IV. Who will do the ugly jobs? V. What about free riders? VI. Won't prices increase? VII. Won't the majority of net recipients just demand more and more UBI from the rich?

UBI Won't Change Anything (The Capitulation Critique)

Counter-intuitively, one of the sharpest polemics against UBI comes from the progressive left. In Daniel Zamora’s brilliant The Case Against a Basic Income, he writes:

“UBI isn’t an alternative to neoliberalism, but an ideological capitulation to it. In fact, the most viable forms of basic income would universalize precarious labor and extend the sphere of the market — just as the gurus of Silicon Valley hope.”

This view builds from Luke Martinelli’s assessment: an affordable UBI is inadequate, and an adequate UBI is unaffordable. If all that’s affordable is a UBI well below the poverty level, then these critics argue that nothing will fundamentally change. An inadequate UBI fails to grant workers sufficient means to reject exploitative jobs, fails to eliminate poverty, and fails to establish the physical basis for voluntary trade. Effectively, all an inadequate UBI would do is provide a cash stimulus to existing markets.

Moreover, even an adequate (poverty level) UBI could function as a capitulation to neoliberalism if it’s conceived as a full replacement, rather than supplement, to existing welfare and social programs. When Milton Friedman proposed his guaranteed income in the form of a negative income tax, this is precisely what he had in mind. Same with Charles Murray’s more recent UBI proposal.

The validity of this critique then relies on two factors: the UBI amount, and how we pay for it.

But as Zamora himself notes, funding an adequate UBI is a question of political, rather than economic feasibility. Of course we could fund an adequate UBI. The capitulation critique does not doubt this. Rather, they doubt that it’s realistic that the necessary taxes could make it through the political process.

The capitulation critique, then, does not apply to a poverty level UBI funded by progressive taxation. It merely doubts its political viability. Far from a nail in the coffin, this points to the conspicuous lack of rigor applied to existing progressive funding proposals for an adequate UBI. If we are to overcome this sense of politically impossibility, we need to put forward realistic funding models.

Won't We Just Become Lazy & Dependent (The Human Nature Critique)

If we manage to fund an adequate UBI, won’t we all just become idlers? Won’t we just waste the free time we’re afforded? Is it worth enacting the largest program in American politics simply to enable people to spend more time watching Netflix and going to the beach?

At heart, this is a question of human nature. How would humans behave if they weren’t compelled to act by the threat of starvation and homelessness? Is human nature fixed, or does it adapt to changing social circumstances?

In fact, this is one of the main divergence points between Adam Smith and Karl Marx. Both believed that society thrives by maintaining an artificial scarcity. But Smith believes maintaining artificial scarcity is the only way to incentivize humans to engage in socially productive activities:

"And it is well that nature imposes [artificial scarcity] upon us in this manner. It is thisdeceptionwhich rouses and keeps in continual motion the industry of mankind. It is this which first prompted them to cultivate the ground, to build houses, to found cities and commonwealth, and to invent and improve all the sciences and arts, which ennoble and embellish human life"

Marx held a more adaptive, evolutionary view of human nature. He believed that how we spend our leisure time is inextricably linked to the working conditions and modes of production present in society. He writes that “all history is nothing but a continuous transformation of human nature.”

Both John Maynard Keynes and Henry George side with Marx on this question. The transformation of material and social conditions, they believe, will lead to the transformation of human behavior. George writes, in what I suspect is a direct counter to Smith:

“But it may be said, to banish want and the fear of want, would be to destroy the stimulus to exertion; men would become simply idlers, and such a happy state of general comfort and content would be the death of progress. This is the old slaveholders’ argument, that men can be driven to labor only with the lash. Nothing is more untrue.”

Worrying that UBI would amplify our idleness, our ‘time wasting’ behaviors, is a fallacy that assumes present behaviors would continue unchanged in radically altered social conditions. It fails to account for how economic distress presently weighs upon, and influences, how workers spend their ‘time off’.

As I’ve written about elsewhere, an adequate UBI must be considered in light of its implications for human development. The kinds of humans we become by living in society would likely change.

But there is a deeper assumption that motivates the human nature critique of UBI: that we have a right to judge how others spend their time.

In terms of UBI, this assumption arises because people’s free time would be, in part, funded by redistributing the earned income of some to all. Do we owe this kind of financial support to each other?

This critique is commonly known as the free rider problem.

The Free Rider Critique

The free rider problem suggests that even if UBI wouldn’t create “universal basic idling”, it isn't fair to redistribute earnings from hard-working citizens towards those who don’t contribute value to society. By receiving tax-funded income without contributing their own labor income to the tax base that funds UBI, they’re ‘free riding’ off the earned income of others. In this view, UBI gives people “something for nothing”.

A poverty-level UBI of $12,490 is hardly a living wage for even the most ascetic of citizens; most will continue to work and earn additional income. However, it is plausible to imagine at least some percentage of the population who choose to live off their UBI alone. It’s more likely to see a proliferation of full-time workers drop to part-time. UBI could make up enough of the difference so that they can maintain relatively similar lifestyles, while generating fewer taxable wages for the overall pot.

How might this criticism change if we apply it to parents who choose to stay home and raise their children? Does the same sense of unfairness come into play when recipients use UBI to fund socially valuable activities that markets fail to compensate? Surely a devoted parent is worth more to society than an unmotivated office administrator, or insurance salesman?

What about aspiring scientists who use the newfound financial and time freedoms to focus on exploring new theories? Or artists who dedicate their time to creativity? In this sense, UBI functions to extend earnings to those engaged in socially valuable pursuits that markets fail to compensate for.

Where free riding turns problematic is the assumption that willfully unemployed UBI recipients will live in ways that do not create value for society. Receiving “something for nothing”. But this is not only assumed, it stands in direct conflict with empirical studies on how UBI affects labor force participation. Even beyond the question of whether UBI would stimulate or stifle economic activity, a larger question looms: are we comfortable letting markets be the judge of what constitutes value?

Using wages as the prime indicator of value-creation solidifies the market's role in determining social value. But much of the progressive left’s movement is about displacing earnings as sole indications of social value. There are forms of value markets systematically fail to recognize, and forms of socially valuable (usually long-term) investments that markets fail to incentivize. Not to mention the forms of negative value that markets stimulate.

In this sense, the free-rider problem might not be a problem at all, but a solution. It functions alongside the market to stimulate forms of social value that markets leave behind.

Another proposed response to the free-rider problem is to shift the narrative frame of UBI. Since progressive taxes that draw from high-earning sectors of society would fund UBI, some claim that UBI is not redistributing the rightful ‘earnings’ of others, but distributes the portion of collective wealth that’s captured by high private earnings. In this sense, UBI is more of a social dividend that formalizes the collective nature of value creation on modern economies.

Consider how this logic of social dividends applies to raising the corporate tax rate, for example. Mariana Mazzucato has demonstrated how much of the iPhone's signature technology is a result of publicly funded R&D. Although taxpayers effectively socialize the risk of this R&D, the financial returns on that investment are privatized, none of which goes back to the taxpayers who (partially) funded the investment.

Should not a small portion of the financial earnings from publicly funded innovation return to those who funded the initial research? Isn’t the public entitled to share in the financial returns on innovations our tax dollars paid for?

Similar logic is at play for many high-earning sectors of society. From Google, Apple, to Tesla, Mazzucato shows how stories of value creation systematically neglect the role of public investment. Framing UBI as a social dividend formalizes the collective nature of value creation, paying dividends on the public’s investment in innovations that spur private fortunes.

A common example is the Alaska Permanent Fund, which taxes all mineral (primarily oil) royalties a minimum of 25%. They reason that Alaskan oil belongs to all Alaskans, rather than whoever manages to dig it up first. Anyone who uses the oil must compensate all other collective owners for excluding them from using it.

The tax revenues are deposited into an investment portfolio that each Alaskan shares an equal share in, receiving annual dividends that fluctuate with the stock market. Applying this logic nationally, Matt Breunig’s proposal for a social wealth fund makes every American an equal shareholder in a collectively owned portfolio.

Framing UBI as a social dividend only makes sense if the funding mechanisms draw from areas of society where large private earnings are bolstered by neglecting public contributions. To sufficiently appease free-rider concerns, UBI advocates must demonstrate what sectors of society wind up paying for UBI under their funding proposals.

Who's Gonna Scrub the Toilets? The Division of Labor Critique

In Zamora’s polemic against UBI, he asks a cutting question: if an adequate UBI gives workers the ability to say “no” to undesirable labor, how can we be sure all the work that needs doing, would get done?

“...a ‘utopian’ [by which he means at least poverty level] UBI raises questions about how the distribution of work — that is, the division of labor — would be determined in a society where we could choose not to work...A “utopian” UBI...simply assumes that in a society liberated from the work imperative, the spontaneous aggregation of individual desires would yield a division of labor conducive to a properly functioning society; that the desires of individuals newly freed to choose what they wish to do would spontaneously yield a perfectly functional division of labor. But this expectation is assumed rather than demonstrated.”

First, it’s worth nothing that by “utopian” UBI, Zamora means a poverty level, or $1,041 monthly UBI. This is hardly enough for even the most ascetic citizens to live on alone. We should certainly expect radical changes to the labor market. But the work incentive, while perhaps marginally dampened, is far from “liberated” by such a UBI.

Liberation aside, Zamora’s point remains. What if nobody chooses to work as a janitor anymore? What if no one is willing to clean the sewers? Unless technology fulfills its promise and automates all of the work humans would rather not do, the full division of labor required to maintain society may include jobs that people, given the means, simply wouldn’t take.

This is one of the greatest fissures in UBI discourse. The ‘work imperative’ is both the glue that holds the system together, and a bleak reality that suffocates working classes. We cannot yet outsource all undesirable jobs to robots. While a work incentive remains even with a poverty level UBI, critical attention must be turned to reflecting on how to maintain the necessary division of labor.

On one hand, David Graeber believes with a UBI, bullshit jobs might simply disappear, because people wouldn’t take them. Alternatively, those unattractive jobs that still require doing for society to function may be forced to offer higher wages. The ways in which wages might respond to UBI lead us into the fascinating territory of the sustainability critique.

The Economic Sustainability Critique

We can imagine that huge amounts of people may choose to drop from full to part-time work, supplementing the gap in income with UBI. On the whole, this may lead to a decrease in taxable wages. As taxable wages decrease, so does the pool of money taxes draw from to fund the UBI.

The magnitude of this decrease depends largely on what kinds of taxes are used to fund the UBI. A system that relies heavily on income taxes would face serious issues with a decreasing taxable wage base. But if UBI were funded with land value taxes, carbon taxes, wealth taxes, consumption taxes, capital gains taxes, etc., UBI’s dependence on taxable wages would be lessened.

Still, what if UBI, by dampening the work imperative, succeeds almost too well in allowing people to engage in more unpaid activities? What if the size of the formal economy shrinks, tax revenues wither, and UBI winds up eroding the very capital flows that sustained it?

There’s a relevant concept in economics known as the Laffer curve. It says that as you increase a tax rate, you'll raise more revenue until a certain point, after which the tax rate is so high that it discourages people from engaging in the activity, and the tax revenues begin to decline.

For example, imagine a carbon tax. If a carbon tax increases the price of gasoline from $2.50/gallon, up to $2.85/gallon, most consumers won’t change their behaviors. They’ll consume just as much gasoline, yielding higher tax revenue.

But if the tax shot the price up to $10/gallon, many consumers would change their behaviors to consume less gas, yielding less tax revenue:

We can apply the Laffer curve to UBI, asking how overall tax revenues respond to the level of UBI. Just like the Laffer curve, beginning with a UBI of 0, we’d have today’s present tax revenue. As the UBI increases to $50, $100, $200, we’d expect tax revenues to increase for two reasons.

First, because of the increased tax revenues required to fund the UBI. Second, a UBI funded by progressive taxes redistributes money from higher ends of the income distribution to the lower. The wealthy are less likely to spend each marginal dollar they receive, while lower income groups are more likely to spend any additional dollar they receive. So we can expect that UBI would stimulate economic activity, leading to more taxable revenue.

But as the UBI increases, the imperative to work decreases, and the progressive taxes required to fund the UBI grow steeper. At some point, we reach the peak of the curve, beyond which overall tax revenues begin to decrease as people stop working, and others cease chasing large fortunes that would just be reclaimed by taxes.

In this case, we’re faced with a design project: find the optimal level of UBI that maximizes the payout without decreasing tax revenue.

But the sustainability question can go a step further. What if we find this optimal balance point that provides a sufficiently high UBI to cover people’s basic needs without eroding its own tax base or tanking the economy. How does the economy change? As we explored in the division of labor section, a high enough UBI threatens to eliminate the incentive to do undesirable work.

In a wonderfully provocative 1986 paper - The Capitalist Road to Communism - Philippe Van Parijs and Robert van der Veen explore this question. Assuming a sustainable and adequate UBI, they hypothesize a “twist” in capitalist logic, whereby wage rates for undesirable work will increase to attract workers, while wages for desirable work will decrease, since people have enough to cover their basic needs and are more free to accept more interesting work for lower pay. “Consequently,” they write:

“...the capitalist logic of profit will, much more than previously, foster technical innovation and organizational change that improve the quality of work and thereby reduce the drudgery required per unit of product.”

How will the twist in capitalist logic create incentives that reduce the “drudgery required per unity of product”? Consider the cost of human labor relative to its automatized equivalent. Presently, it’s usually cheaper to hire human workers than invest in the machinery and automation that can perform equivalent work. But already, we’re seeing roaming robots replace supermarket workers, self-driving cars replacing drivers, and tablets replacing waiters at restaurants.

If this twist of capitalist logic drives up the wage rate for undesirable work, the cost relation will flip. It will become more expensive to hire humans at higher wages where machines can do the equivalent labor. The costs of automation will become a rational choice for capitalists when the equivalent cost of labor surpasses it.

These are uncertain speculations, to be sure. And the assumption that there exists an optimal level of UBI that covers basic needs without grinding down its own tax base is little more than an assumption. We have economic models that suggest UBI would decrease growth, while others say just the opposite.

In the face of these uncertainties, we may nevertheless rest assured that UBI would fundamentally change the economy, and in so doing, the kinds of lives we lead. We should speculate as widely as possible, and survey the many possibilities as diligently as we can.

If we can conclude anything from these concerns and speculations, perhaps it’s that moving in the direction of UBI merits prudence. While we must understand that how the economy responds to a $250 UBI cannot be extrapolated to suggest its response to a $1,000 UBI - the two are fundamentally different - we do have the option of moving towards UBI, rather than diving straight into the unknown.

The "Won't UBI Inflate Prices?" Critique

If everyone receives an extra $12,490 annually, won’t producers raise prices to absorb this extra capital? Won’t landlords raise rent, retail stores raise prices, ultimately absorbing the UBI entirely such that no meaningful changes remain?

In brief: maybe a little bit, but probably not much.

Inflation is not so simple as: people receive more money, therefore producers increase prices. Inflation only occurs when aggregate supply is unable to keep up with increasing demand. So long as people’s purchasing power increases, and supply can scale to match, there is no inflation.

Moreover, most UBI proposals do not even propose to increase the money supply. UBI funded by progressive taxes just shuffles existing money around. But even if a UBI were funded entirely by printing the requisite $3.6 trillion every year and adding it to the economy, it’s not clear how much inflation would actually occur.

While prevailing logic assumes such an action would cause so much inflation as to render the idea obviously detestable, the matter is far from obvious. For example, Ellen Brown writes that, by virtue of how money is created, “our money supply is in a chronic state of deflation.” When banks approve a loan, that money is created and assimilates into the economy. But the subsequent interest owed is not created, so money creation always furthers the deficit that divides money owed from money circulating in the economy.

This gap between debt owed and the money supply creates a buffer against inflation. Any increase in the money supply that closes this gap (i.e., UBI money used to pay existing debts) causes no inflation.

But few UBI proposals rely on deficit spending - most use progressive taxes to redistribute money downwards. In this case, the money supply does not increase, but spending patterns and purchasing power do.

The lower on the income distribution one falls, the higher their propensity to spend each additional dollar they receive. So if progressive taxes redistribute money downwards via UBI, we can expect aggregate spending in the economy to increase. So long as supply can scale up to match increased demand, no inflation occurs.

Inflation only occurs when supply hits its maximum, and increasing demand cannot be matched by increasing supply. So the degree to which the economy can increase its supply also provides a buffer that absorbs inflation.

For example, since 1982, every Alaskan citizen has received a partial UBI through taxes levied on oil revenues. Each year, citizens receive anywhere from $1,000 - $2,000. From the introduction of their partial UBI to the present, Alaska has experienced lower inflation than the rest of the nation. This, despite every citizen receiving an extra ~$1,500 annually.

Similar results were found when the Mexican government conducted experiments across a network of villages. Villages where people received direct cash transfers experienced no statistically significant changesin prices.

Results from the Alaska, or rural Mexican villages can only tell us so much about how the entire US economy would react to a UBI. A more representative study looked specifically at how a UBI funded by progressive taxation (specifically, by progressive income taxation, which is a more distortionary UBI than most proposals that use forms of taxation other than excessive income taxes) would affect housing prices in New York City. They find that a $5,000 household UBI (another departure from actual UBI proposals, that distribute benefits per individual) would increase aggregate welfare of the bottom 50% of the wealth distribution. Most notably, they find that this UBI would actually decrease housing prices.

All models should be taken skeptically, as there always exists inherent limitations in our ability to actually model UBI. Not to mention the varying assumptions required to construct models that often differ from the actual UBI proposals these models are used to evaluate. Nevertheless. Each successive experimental context related to UBI and inflation suggests the same finding: there is no obvious causality between unconditional income transfers and price inflation.

The Political Tyranny Critique

Another common concern goes like this: funding a UBI requires progressive taxes that fall mostly on the wealthy. But the wealthy constitute only a minority in society. If the majority of society are net UBI recipients, meaning they receive more in UBI than they pay in increased taxes, what’s to stop them from leveraging their majority and voting to raise the level of UBI, exploiting the rich minority?

This concern can be handled in the same way we handle voting for presidential impeachment, an event too important to leave up to mere majority rule. For the senate to impeach a president, they require a supermajority consensus. This is just a higher threshold of consensus than other measures require. Requiring a supermajority to change UBI levels can help prevent partisan exploitations and tyrannical majorities.

How to Pay for UBI

At the moment, how to pay for UBI is the most important question of the discussion. There’s plenty of theory, there are well-reasoned arguments on all sides. What we need to develop are realistic funding proposals that we can subject to scrutiny.

The relevant question isn’t can we pay for UBI, but should we pay for UBI. Of course we can. We could finance the entire program through deficit spending, just creating the money and handing it out (as banks do daily when approving loans). But that probably isn’t a good idea, because the inflationary consequences of doing so likely outweigh the benefits.

How we pay for UBI determines everything from how economic incentives change, to whether it functions as a floor or ceiling for social policy. A handful of proposals for UBI exist, but they mostly lack the attention to detail that enables a transition from politically impossible to politically viable.

No single tax is sufficient to fund UBI. Raising $3.6 trillion in revenue requires a coalition of progressive taxes. But this also presents an opportunity to meaningfully redesign and update economic incentives for the 21st century.

Here, I’ll gather a list of relevant taxes and strategies, together with revenue projections. There is no agreement on how much a wealth tax, for example, would raise. So I’ll include the range of revenue projections, from conservative skepticism to passionate optimism.

Background: According to research by Emmanuel Saez and Gabriel Zucman, 2018 marked the first time the wealthiest members of society paid a lower effective tax rate than the poorest:

The conversation on how to implement a more progressive tax system is now booming. One facet of the broader project of progressive taxation is marginal income tax rates. Marginal income tax rates in America on the highest income groups used to exceed 90% (with effective rates closer to 60%), while today, the highest bracket faces a tax rate of 37% (with far lower effective rates). All incomes above $400,000 are treated to this same rate.

Research by Zucman, Saez, and Stantcheva (2014) attempts to derive the optimal top rate of taxation to maximize revenue, in relation to the Laffer curve for income taxes. They find that a rate of 83% on the highest incomes maximises revenue.

But recent progressive proposals to simply add an 8th bracket on incomes above $10 million leave the space between $400,000 and $10 million unchanged. We need more nuance in how we tax incomes.

A first-principles approach might draw from the idea of a monotonically increasing tax rate that does away with brackets altogether. Every additional dollar earned is subjected to a slightly higher tax rate, achieving a truly progressive tax on income that adheres to Adam Smith’s original guideline:

“The subjects of every state ought to contribute towards the support of the government, as nearly as possible, in proportion to their respective abilities; that is, in proportion to the revenue which they respectively enjoy under the protection of the state.”

But to avoid such predictable responses to higher income tax rates as capital flight and fiscal manipulation (realizing earnings as capital gains rather than personal income to avoid higher tax rates), any progressive income tax must be part of a broader program of tax reform.

Raising and reforming capital gains taxes

Projected revenues: $6 billion - $170 billion.

Examples: Shifting to a carryover tax basis is projected to raise $10.4 billion annually, and taxing capital gains of the top 1% on an accrual basis could yield $170 billion. These projections are for changing methodology, rather than raising rates.

Revenue projections for raising capital gains rates are complex, because outcomes depend on the broader system of taxation. As such, models that predict a $6 billion annual raise in revenue by raising capital gains taxes from 20% to 24.2% are tenuous.

Background: Capital gains are the second most prevalent mode of realizing income, functioning in tandem with labor income taxes. This is why considering capital gains and income taxes alongside each other is so important: at upper levels of the income distribution, gains are often transferable between these two categories.

Wealth tax

Projected revenues: $118 billion - $375 billion.

Example: A 2% tax on wealth above $50 million, cranking up to 3% on wealth above $1 billion, is projected to raise $275 billion, annually.

Background: Many European countries tried wealth taxes, most proved ineffective. Recent economists advocating for a wealth tax acknowledge that we must learn from these failures to design an effective wealth tax.